Overview

CHIA collects annual commercial health insurance premiums data from health care payers, providing insights into the costs faced by both Massachusetts employers and employees. CHIA also monitors high-deductible health plan enrollment and consumer cost-sharing over time. These measures are reported in CHIA’s Annual Report on the Performance of the Massachusetts Health Care System.

Key Findings

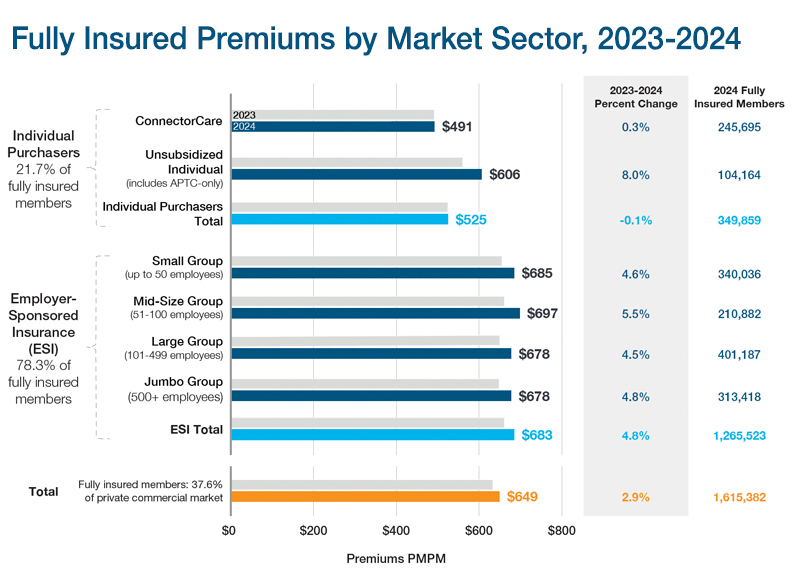

2.9% growth in 2024

for fully insured premiums

This was slower than prior years (5.9% in 2023), driven by enrollment shifts in the individual purchaser sector to lower-premium ConnectorCare plans. Premiums for individual purchaser plans declined 0.1% overall while premiums for employer-sponsored plans increased 4.8%.

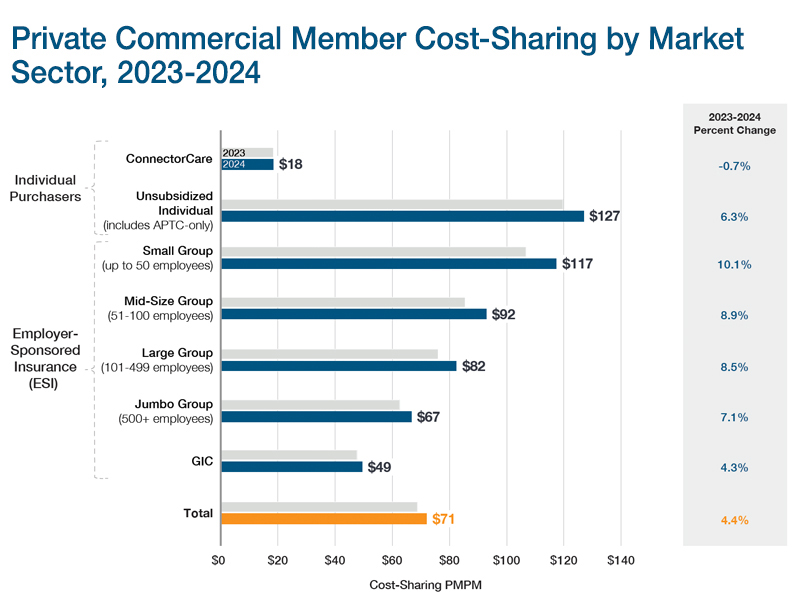

8% increase in 2024

for member cost-sharing

Among small and mid-size employer groups, employers and employees faced heightened cost pressures: member cost-sharing was highest for these employees ($117 PMPM and $92 PMPM, respectively) and these employer groups also had the highest premiums.

90.7% of premiums

were used to pay for members’ medical care

In 2024, the remaining 9.3% went toward non-medical expenses and payer surplus; this proportion was smaller than in the 2 prior years and similar to 2021.

Commercial Insurance Premiums

Commercial insurance premiums are costs shared by individuals and employers. In Massachusetts, 91.9% of people with commercial insurance are enrolled in employer-sponsored plans. In these plans, both the employer and the employee contribute toward the cost of coverage.

Health care payers use these premiums to pay for members’ medical care. They also use a portion of the premium to cover administrative costs, reserves, commissions, taxes, and other expenses.

Premiums are set ahead of time based on past data and expected future costs. For example, premiums for plans offered in 2024 were set in early 2023 using spending data from prior years (mainly through 2022) and projections of future changes in health care use and costs.

In Massachusetts, payers must meet minimum medical loss ratio (MLR) requirements. This means they must spend at least 88% of premiums on medical care in the merged market (individuals and small employers) and 85% for large employer plans. These rules help limit administrative spending, especially when actual costs are lower than expected.

Commercial Insurance Member Cost-Sharing

Commercial insurance member cost-sharing includes the medical costs that a member must pay out of pocket. This includes deductibles, copays, and coinsurance—costs not covered by the payer, employer, or state subsidies.

CHIA reports on member cost-sharing by market sector, product type (such as HMO, PPO, and POS), funding type, and benefit design (such as high-deductible, tiered network, and limited network plans).

CHIA also includes cost-sharing and affordability findings from the Massachusetts Health Insurance Survey (MHIS) and the Massachusetts Employer Survey (MES). MHIS reflects how medical costs affect Massachusetts residents across all types of coverage. MES focuses on cost-sharing and decision-making in the employer-sponsored insurance market.

CHIA’s Annual Report includes members with little or no medical spending as well as those with high medical costs. The data does not include out-of-pocket spending for services not covered by insurance, such as over-the-counter medicines or standalone dental and vision care. Cost-sharing estimates also don’t account for employer contributions through health reimbursement arrangements or health savings accounts.

Recommended Links

Annual Report

Statewide THCE totaled $83.3 billion or $11,663 per person in 2024, a 5.7% increase from 2023, according to CHIA's latest Annual Report on the Performance of the Massachusetts Health Care System.

Massachusetts Health Insurance Survey (MHIS)

Analyses from CHIA's statewide resident survey on insurance coverage, access to care, affordability, and health care experiences.

Massachusetts Employer Survey (MES)

Analyses from CHIA's employer survey on health insurance offerings, costs, plan design, and coverage trends.